We need to reduce the value of the inventory by $150 to reflect the discount received. Now, we have all the information we need to complete the second entry. We will look at this transaction under both methods so you can see the difference. Before we start looking at each method, let’s start by discussing what is the same under each of the methods.

- A contra expense account is an account used to reduce the amount of an expense without changing the balance in the main expense account.

- The purpose of the Sales Returns account is to track the reduction in the value of the revenue while preserving the original amount of sales revenue.

- This can help anyone viewing the financial information to find the historical cost of the asset.

- Net sales is equal to gross sales minus sales returns, allowances and discounts.

- Obsolete, Unsold and Unusable Inventory are contra asset accounts with a credit balance that reduce the normal debit balance of the main Inventory asset account in order to present the net value of inventory on a company’s balance sheet.

How to Calculate Straight Line Depreciation

Therefore, we should never use the inventory account in purchase transactions for companies that use the periodic method. When the company pays the cost of having the flyer printed, a journal entry is done. The purpose of the Sales Returns account is to track the reduction in the value of the revenue while preserving the original amount of sales revenue. A buyer debits Cash in Bank if a purchase return or allowance involves a refund of a payment that the buyer has already made to a seller. A buyer debits Accounts Payable if the original purchase was made on credit and the payment has not yet been made to a seller. Medici Music purchased instruments to sell in its stores from Whistling Flutes, LLC on August 13.

Asset Contra Account

Contra account is important as it not only allows a company to report the original amount of a transaction but also report any reductions that may have happened so that the net amount will also be reported. They are useful in preserving the historical value in the main account while presenting a write-down or decrease in a separate contra account that nets to the current book value. In the accounting general ledger, the credit balances of the contra purchase expense accounts reduce and offset the usual debit balances reported in the standard purchase expense accounts. Another allowance that reduces accounts receivable is the allowance for sales returns and discounts. This account operates in a similar fashion to the allowance for doubtful accounts. The most common example of an allowance in accounting is the allowance for doubtful accounts.

Understanding Contra Liability Accounts

After 30 days, your payment is now late and the seller can add on late charges or interest, depending on state law. The purpose of the Owner’s Withdrawal account is to track the amounts taken out of the business without impacting the balance of the original equity account. A purchase allowance is a reduction in the buyer’s cost of merchandise that it had purchased. The purchase allowance is granted by the supplier because of a problem such as shipping the wrong items, the incorrect quantity, flaws in the goods, etc.

Revenue Contra Account

The contra account purchases returns and allowances will have a credit balance to offset it. Bill uses the purchases returns and allowances account because he likes to keep tabs on the amount as a percentage of purchases. He also needs to debit accounts payable to reduce the amount owed the supplier by the amount that was returned. Net sales is what remains after all returns, allowances and sales discounts have been subtracted from gross sales.

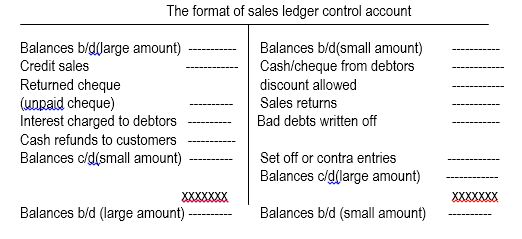

Chapter 14 — Control Accounts

For example, a purchaser brought a $100 item, with a purchase discount term 3/10, net 30. If he pays half the amount In accounting, gross method and net method are used to record transactions of this kind. Under the gross method, the total cost of purchases are credited to accounts the contra account purchases discount has a normal debit balance. payable first, and discounts realized later if the payments were made in time. Bills payable or notes payable is a liability that is created when a company borrows any specific amount of money. If the company repays the loan early, the lender may provide a discount.

Of that amount, it is estimated that 1% of that amount will become bad debt at some point in the future. This means that the $85,000 balance is overstated compared to its real value. At this point, it isn’t known which accounts will become uncollectible so the Accounts Receivable balance isn’t adjusted. Instead, an adjusting journal entry is done to record the estimated amount of bad debt. When working with discounts, we generally calculate the discount and record it at the time of payment.

If a firm sells a high volume of a product on credit, it is likely that some of its customers will not be able to pay their credit payment. The contra asset account Accumulated Depreciation is deducted from the related Capital Assets to present the net balance on the parent account in a company’s balance sheet. The mechanics of the allowance method are that the initial entry is a debit to bad debt expense and a credit to the allowance for doubtful accounts (which increases the reserve).

This discount is subtracted from the total amount borrowed to better reflect the discount given by the lender. A company creates allowances for doubtful accounts to record the portion of accounts receivable which it believes it will no longer be able to collect. The amount in allowance for doubtful accounts is deducted from the accounts receivable account of a company. A contra account is also known as a valuation allowance, because it adjusts the carrying value of the account with which it is paired. To account for this, accountants have to estimate non-payments with the use of doubtful accounts.

Charlene Rhinehart is a CPA , CFE, chair of an Illinois CPA Society committee, and has a degree in accounting and finance from DePaul University. Examples of deferred unearned revenue include prepaid subscriptions, rent, insurance or professional service fees. We strive to empower readers with the most factual and reliable climate finance information possible to help them make informed decisions. Our goal is to deliver the most understandable and comprehensive explanations of climate and finance topics.